We help Business Owners & Directors turn company wealth into personal wealth.

Shortlisted for Broker of the Year 2023 🏆

Extract Wealth From Your Business

We've helped clients from some of Ireland's largest companies

Extracting wealth from a company

There are 3 main options for a business owner to extract profits from their Company:

1. Through a salary

Probably the most obvious and most popular way of extracting wealth from a business is through a salary or dividends.

However, it’s not attractive from a taxation point of view. Income Tax, PRSI and USC mean it could be as high as 52% tax.

Probably the most obvious and most popular way of extracting wealth from a business is through a salary or dividends.

However, it’s not attractive from a taxation point of view. Income Tax, PRSI and USC mean it could be as high as 52% tax.

2. Leave profits within the company

Although it’s a risk and circumstances may change. You’ll also be liable to a Corporation Tax of 12.5% on all profits.

Although it’s a risk and circumstances may change. You’ll also be liable to a Corporation Tax of 12.5% on all profits.

3. Extract wealth through a pension arrangement

The final option when extracting wealth from a business is through pension arrangements.

The final option when extracting wealth from a business is through pension arrangements.

Contributions to a pension arrangement offers some key benefits:

- Tax relief on contributions at your marginal tax rate

- Tax-free growth

- Tax-free sum at retirement

We can help you with:

Executive Pensions

Are you a director of a company and looking to start a pension?

Self-Employed Pensions

Our clients include both self-employed and sole traders assessing their options.

Personal Retirement Savings Account (PRSA)

This is a personally owned pension that can be taken out regardless of employment status.

Our accreditations

At Pension Support Line, our advisors come with a wealth of experience and accreditations.

From being Certified Financial Planners to lecturing for the Retirement Planning Council of Ireland, we pride ourselves on our experience and expertise.

Invest with the experts

At Pension Support Line, we take pride in our strong partnerships with some of Ireland’s leading financial providers.

This network of esteemed companies enhances our ability to offer you a broad range of high-quality investment options and services. Here are the key benefits you’ll enjoy as a result of these collaborations:

- Diverse Investment Choices

- Competitive Rates and Terms

- Enhanced Market Insights

- Tailored Financial Solutions

What is an Executive Pension Plan?

An Executive Pension Plan is a scheme designed to help company owners and company directors save for retirement.

These plans allow you to appropriately save for retirement in a tax-efficient manner.

As with other pension arrangements, members of the Executive Pension Plans can avail of all the tax incentives pension schemes have to offer.

Who is eligible to take out an Executive Pension Plan?

Executive Pension Plans are designed for company directors and senior management.

Although, technically, anyone who is taxed under Schedule E is eligible. You can use income earned from this employment as contributions to your Executive Pension Plan.

Any income earned outside of this Schedule E tax bracket will not be eligible as contributions to your arrangement.

| Schedule D – Case I |

| Schedule D – Case II |

| Schedule D – Case III |

| Schedule D – Case IV |

| Schedule D – Case V |

| Schedule E |

| Schedule F |

For example, any rental income or dividends from shareholdings falls outside the eligibility criteria.

What advantages does an Executive Pension Plan have over other pension arrangements?

An Executive Pension Plan provides you with many benefits over other traditional pension arrangements. One of the main benefits is the ability to contribute a higher percentage of your income whilst receiving tax relief.

Below we have compared people with identical details. One has an Executive Pension Plan while the other has a Personal Retirement Savings Account (PRSA).

| Age | Retirement Age | Pension Arrangement | Percentage of salary allowable for contribution |

| 42 | 65 | PRSA | 25% |

| 42 | 65 | Executive Pension Plan | 76% |

We can see from the table above that there is a significant difference in the level of contributions allowed. An individual of the same age and gender can contribute 51% more of their salary to an Executive Pension Plan whilst still receiving tax relief.

| Male | Retirement Age | |

| Current Age | 60 | 65 |

| 30 | 72% | 54% |

| 35 | 86% | 63% |

| 40 | 108% | 76% |

| 45 | 144% | 95% |

| 50 | 216% | 126% |

| 55 | 432% | 189% |

| Female | Retirement Age | |

| Current Age | 60 | 65 |

| 30 | 67% | 49% |

| 35 | 80% | 58% |

| 40 | 100% | 69% |

| 45 | 133% | 86% |

| 50 | 200% | 115% |

| 55 | 400% | 173% |

As a director or company owner, this can be a huge advantage and an extremely tax-efficient way of saving for retirement.

An Executive Pension Plan also has other advantages such as:

- Contributions can be fully funded through the company.

- Corporation tax-relief available.

- No USSC or PRSI on employer contributions,

- Eligible to access benefits from age 50

- 25% tax-free retirement lump sum.

If you would like to discuss options regarding starting or reviewing a current Executive Pension Plan, feel free to contact our team.

Example of contributions to an Executive Pension Plan

Pension contributions to an Executive Pension Plan will be eligible for tax relief. Below we look at some examples of how this tax relief is applied.

| Name | Monthly Contribution | Tax Relief (40%) | ‘Real’ Cost |

| Jean | €950 | €380 | €570 |

| Brian | €1300 | €520 | €780 |

| Catherine | €2,500 | €1,000 | €1,500 |

It is worth noting that for the above example, all contributors are in the 40% income tax bracket.

A major advantage is that these contributions will be allowed to grow tax-free. It can be hard to calculate the growth exactly, but below we have looked at a popular fund and how it has performed over the past 10 years.

| Company | Zurich |

| Fund Name | Zurich Dynamic Fund |

| Risk Rating | 5 |

| Features | High equity content |

The above shows the performance of Zurich’s dynamic fund since 2001. We can see how it fluctuates year on year but overall has a solid performance.

If we focus on the past 10 years for this example, we see it has seen growth of on average 12.18%.

Combine this with compound interest, tax-free growth and a 25% tax-free sum at retirement and an Executive Pension Plan is an attractive option.

At what age can you access an Executive Pension Plan?

You will be eligible to access the benefits from your Executive Pension Plan from age 50 Although, in certain circumstances, you may be able to access benefits earlier.

However, this will only be the case if you can no longer work due to illness if you retire.

Below we break down at what age you can access your benefits from different types of pension arrangements.

| Pension Type | Age you can access benefits from |

| Executive Pension Plan | 50 |

| Personal Pension | 60 |

| Personal Retirement Savings Account (PRSA) | 60 |

| Occupational Pension Scheme (DB/DC) | 50 |

It is also worth noting that specific occupations such as sports professionals may qualify for early retirement.

Does your company shareholding percentage affect the age you can access benefits?

Yes. Your shareholding within the company will directly impact at what age you can retire.

This is important as many directors look to retire early when possible. However, your percentage of shareholding will likely play a role in this decision.

Normal Retirement age for 20% Directors

As a 20% Director, the normal retirement age must be between ages 60 and 70.

However, in some cases exceptions are allowed although these are subject to Revenue approval.

Early Retirement age for 20% Directors

Early retirement is allowed from age 50. However, in the case of a 20% Director, the Director must sever all links with the employer company.

This includes the disposal of all shares held within the company. A disposal of shares to a spouse or children will not satisfy this requirement.

However, a disposal to an adult child working within the business is allowed.

This particular area requires specific knowledge and experience. If you would like to discuss your options with an advisor, we offer a complimentary consultation.

How can Executive Pension Plan benefits be withdrawn?

Essentially will have two options:

Option 1

- A once-off lump sum up to one and a half time’s final salary*&

- The balance of the fund must then be used to purchase an annuity

Option 2

- A once-off lump sum of up to 25% of the value of the fund &

- The balance of the fund must be used to fund an AMRF and/or ARF

It is important to withdraw your benefits in the way that best suits your needs and circumstances. There may be various options available. Take time, consider all potential avenues, and choose what suits you best.

Extracting wealth from your business

An Executive Pension Plan is a useful way of extracting wealth from a business in a tax-efficient manner.

A combination of tax relief on pension contributions, tax-free growth, and a tax-free lump sum at retirement make Executive Pension Plans a popular choice among company directors.

You will also have the option to fund retirement income via an annuity or Approved Retirement Fund (ARF).

An Executive Pension Plan is just one way to extract wealth from a business. However, there are alternatives. Below we look at three different ways you may choose to extract wealth from your business.

For this example we use a 45-year-old looking to retire in 15 years. We will assume they have €100,000 gross profits. The three options are:

- Leave profits in the business

The first option may be to leave the profits within the business. However, these profits will be liable to corporate tax.

| Initial Investment | €100,000 |

| Less:12.5% (Corporation Tax) | €12,500 |

| Less: income tax, PRSI & USC | €0 |

| Balance | €87,500 |

2. Take profits as a salary

Another option when extracting wealth from a business is to simply take it as a salary. However, this will have significant tax implications as we see below.

| Initial Investment | €100,000 |

| Corporation Tax | €0 |

| Less: income tax, PRSI & USC | €52,000 |

| Balance | €48,000 |

3. Fund an Executive Pension Plan

The third and often most popular option, is to fund an Executive Pension Plan.

|

Initial Investment |

€100,000 |

| Corporation Tax | €0 |

| Less: income tax, PRSI & USC | €0 |

| Balance | €100,000 |

While keeping transparency front of mind, it is worth noting that the Executive Pension Plan will be liable to income tax, PRSI, and USC at the withdrawal stage. However, you will also likely withdraw 25% of the fund tax-free and experience tax-free growth in the interim.

Overall, an Executive Pension Plan can be an excellent, tax-efficient way of extracting wealth from your business. We help clients in such situations assess options and put a roadmap in place.

Book your consultation to arrange a chat and discuss potential options.

5 Reasons starting Executive Pension Plan is a good idea

There are several reasons why starting an Executive Pension Plan is a good idea. The government has put various incentives in place.

There is also a personal element where it allows us to support ourselves financially in retirement. Below are some of the top reasons to contribute to an Executive Pension Plan:

1.Tax relief

One of the most attractive elements of contributing to a pension plan is the fact you receive tax relief on contributions.

These contributions are paid at your marginal tax rate. For example, if you pay 40% income tax, you will receive 40% tax relief on your pension contributions.

| Pension Contribution (per month) | Tax Relief | ‘Real’ Cost |

| €500 | €200 | €300 |

As we see above, the net or ‘real’ cost of your contributions will significantly reduce after-tax relief.

The amount you can contribute whilst receiving tax relief will relate to your age. We have broken down these thresholds below.

| Male | Retirement Age | |

| Current Age | 60 | 65 |

| 30 | 72% | 54% |

| 35 | 86% | 63% |

| 40 | 108% | 76% |

| 45 | 144% | 95% |

| 50 | 216% | 126% |

| 55 | 432% | 189% |

| Female | Retirement Age | |

| Current Age | 60 | 65 |

| 30 | 67% | 49% |

| 35 | 80% | 58% |

| 40 | 100% | 69% |

| 45 | 133% | 86% |

| 50 | 200% | 115% |

| 55 | 400% | 173% |

2. Tax-free growth

Pensions are a unique Investment in that they accumulate free of tax. With other investments, you may be at the mercy of income tax, Capital Gains Tax, or Deposit Interest Retention Tax (DIRT).

Your pension arrangement will avoid all of the above tax implications.

3. Tax-free lump sum

As well as tax relief and tax-free growth, you will likely be eligible to withdraw a percentage of your benefits as a tax-free lump sum at retirement.

Most people will be eligible to withdraw 25% of their benefits tax-free.

There are certain limits in place. As of January 2011, the maximum tax-free lump sum in Ireland is €200,000.

Below we look at some examples of the tax-free lump sum process.

| Name | Pension Fund Value | 25% Tax-Free Lump Sum | Remainder |

| Oliver | €775,000 | €193,750 | €581,250 |

| Amelia | €322,000 | €80,500 | €241,500 |

| Henry | €995,000 | €248,750 | €746,250 |

The ability to withdraw a percentage of your fund at retirement is a huge incentive. It is worth noting there are factors such as redundancy that may affect eligibility.

If you are unsure whether you qualify for a tax-free lump sum, please contact our team.

4. We are living longer

Thankfully we are living longer, healthier lives than ever before. A combination of healthier lifestyles and improvements in medical treatments means most of us live into our 80’s.

However, this increased lifespan also presents other problems. We need money to survive and live out our retirement years the way we would like.

How much you will need to retire will vary from person to person.

Although, our survey showed people would like on average €433,000.

Speaking with your advisor regularly and planning appropriately is the best way to ensure you can enjoy the retirement lifestyle you would like.

5. Could you survive on the State Pension?

As more and more people take advantage of pensions, luckily this means less people are planning to rely on the State Pension.

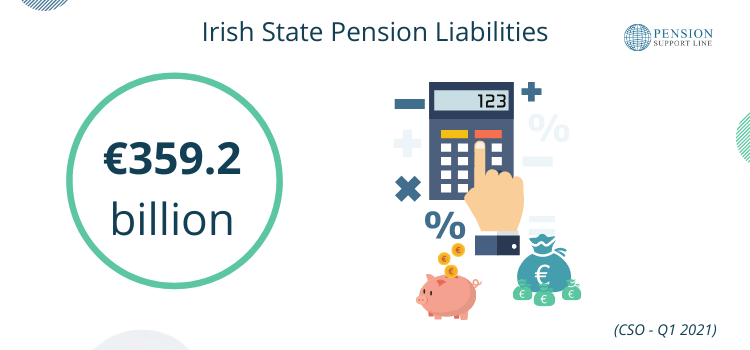

The State Pension is a modest €248.30 per week which does not make it an attractive option for most.

It is also a system with mounting liabilities approaching €360 billion. Combine this with Ireland’s aging population and it is a system that will struggle into the future.

Contributing to an Executive Pension Plan can allow you to plan for retirement. It will also allow you to take advantage of the benefits and tax incentives mentioned above.

How an Executive Pension Plan can benefit an employer

It is not only employees that can take advantage of the benefits an Executive Pension Plan has to offer.

Below are some points to note from an employers/company perspective.

- Company contributions to Executive Pension Plans are deductible for Corporation Tax as a business expense. However, on once-off large contributions, this may need to be spread across a number of years.

- Company contributions to the plan are not subject to benefit-in-kind for income tax purposes. This means you will have no income tax, PRSI, or Universal Social Charge liabilities on the company contributions.

The above illustrates the tax incentives available for contributing to Executive Pension Plans. If you are a company looking to assess your options, we offer a complimentary consultation.

What fund choices are available through an Executive Pension Plan?

With an Executive Pension Plan, you will have various fund choices available. Depending on the life insurance company, they each will have different investment opportunities.

Sitting with your broker and comparing the market is usually a good starting point. From here you can choose a life insurance company along with the exact funds you would like to invest in.

Asset classes

Your investment options will likely be broken down into the five main asset classes which are:

- Cash – These investments will earn short-term interest and have ease of access.

- Property – This often includes commercial property such as office buildings.

- Equities – These are shares in companies. Often global companies where shares are bought and sold on the stock market.

- Bonds – These will often be split between Corporate and Treasury(Government) bonds.

In some cases, you may have alternative investment options such as gold, copper, water infrastructure, agriculture, or green energy.

If you would like a more diversified investment structure, contact our team to discuss potential options.

Type of fund management

When it comes to managing your Executive Pension Plan, there are two main options.

Active Funds

These are ‘actively’ managed by a fund manager. These will act on your behalf to attempt to maximise gains.

Passive Investment Funds

This is where you try to anticipate and identify opportunities. With this type of fund, you will usually buy across a wide range of assets and get a general view of the market.

Neither fund is guaranteed to return a particular level of investment. Choose an investment strategy that best suits your needs and long-term goals.

Attitude to risk

As with any investment, there is a certain level of risk involved. However, you will have options as to which end of the scale you’d like your investment to sit.

Most people are happy to pick a fund choice or a split where their investment will increase slightly over the long term. However, values can decrease and there is always a chance your investment may go down as well as up.

Above we see the risk ratings on a scale from 1-7. European Union law requires that all life insurance companies use a scale that indicates the level of risk of each of their funds.

However, it is important to note that although the numbers are universal, each company takes different factors into account when compiling its scale.

Therefore, the numbers are not like for like. Consult with an expert before making any decision and complete a risk assessment.

Executive Pension Plan fees and charges

All pension arrangements are subject to fees and charges. These help cover the cost associated with running the scheme.

However, some are higher than others and can have a significant impact on your pension fund.

Below we look at some typical terms you may find.

Annual Management Charges (AMC)

These are generally applied as a percentage of your overall fund value. Again, this can differ from arrangement to arrangement.

A typical AMC would be between 0.5% to 1%.

| Total Fund Value | Annual Management Charge | Cost Per Year |

| €850,000 | 0.5% | €4,250 |

Allocation rate

The allocation rate is the percentage of your money that is used to buy units in a pension or investment fund.

For example, if your allocation rate is 98%, for every €100 you invest, €98 is actually used to buy units.

Exit Penalties

In some cases, you may be penalized for withdrawing funds before a certain time period has lapsed.

These charges are referred to as exit penalties. Any potential exit penalties will be outlined in your policy and should be highlighted by your advisor before a policy starts.

Fund switching

In certain arrangements, there may be an administration charge levied should you wish to change funds. However, in most arrangements, you will be allowed a certain amount of free fund switches per year.

Are Small Self-Administered Pension Schemes different to Executive Pension Plans?

A Small Self-Administered Pension Scheme (SSAS) differs from an Executive Pension Plan.

Where a Small Self-Administered Scheme differs, is how and where the contributions are invested. With a Small Self-Administered Scheme, contributions are invested through a Pensioner Trustee company rather than through a life insurance company.

A major benefit of a Small Self-Administered Scheme over an Executive Pension is it may give you a wider choice of assets to invest in.

If you feel you may be suitable for such a scheme, it may be worth consulting with an advisor.

Should I review an active Executive Pension Plan?

Yes. It is important to annual review any type of pension arrangement. This will allow you to appropriately plan and help ensure you reach a number you would like in retirement.

Even what seems like an insignificant difference in fees can have a dramatic impact over a long period. As pensions are often over 25-30 years, these details are important.

Below we look at an example of what a change in AMC can have over a 30 year period.

Let us look at a practical example of how fees & charges can affect your pension fund

We will take someone contributing to their fund over a 30-year period. We will also assume both will receive a 100% allocation rate.

Scenario 1

| Monthly Contributions | €500 |

| Policy fees (annual) | €60 |

| AMC | 1.5% |

| Period | 30 years |

| Annual return | 4% |

| €264,297 |

Scenario 2

| Monthly Contributions | €500 |

| Policy fees (annual) | €0 |

| AMC | 0.25% |

| Period | 30 years |

| Annual return | 4% |

| €329,308 |

Difference

| Total cost of fees & charges | €65,011 |

It is worth noting, the above should not be taken as advice. Amounts will vary due to income tax brackets along with other variables.

How are contributions made to an Executive Pension Plan paid?

You will have the option to pay either regular or single contributions to the Executive Pension Plan. Contributions are taken at source and are eligible for tax relief.

Many directors like to take advantage of regular contributions as well as the lump sum option towards year-end.

How do you set up an Executive Pension Plan?

An Executive Pension Plan is set up under trust meaning the arrangement is legally separate from the business.

This gives Directors and key stakeholders the opportunity to build wealth independent of the business.

Once the arrangement is in place, you will have the opportunity to make regular or once-off payments.

We have experience in helping clients from a wide range of industries start Executive Pension Plans. If this is an area you would like to discuss, feel free to contact our team.

We offer the opportunity to chat through potential options you may have.

Reviewing your existing Executive Pension Plan

If you currently have an EPP and would like it reviewed our team can assist. If you are thinking of having your plan review, it might be a good idea if you cannot answer the following questions:

- What are your annual management charges?

- How has your fund performed in the past 5 years?

- What asset classes is your fund invested in?

If you are not able to answer any of the above it might be worth contacting our team. Having an industry expert take an unbiased view of your plan is never a bad idea.

Next Steps?

We assist clients from a wide range of industries to save for the future while doing so in a tax-efficient manner. If you would like to discuss potential options, feel free to avail of our complimentary consultation.

Our clients range from Directors of SME’s to major shareholders in some of Ireland’s largest companies.

We also assist clients in the process of extracting wealth from their businesses.

You can leave your contact information below or contact our team directly.

Not sure what you need?

Many of our clients were initially unsure of exactly what their options were. Feel free to reach out to our chat box or even pop us over an email with any questions and we will get back to you as soon as possible.

Email: info@pensionsupportline

Types of Consultations Available?

In-Person Consultation

After an initial conversation, an in-person meeting is usually the next course of action.

Learn MoreInformation Hub

In late 2022, there were some important changes to pension legislation. Personal Retirement Savings Accounts…

Frequently Asked Questions

How are contributions made to an Executive Pension Plan paid?

Members have the option to pay either regular or single contributions to the Executive Pension Plan. Contributions are taken at source and set up through the employer’s payroll system.

The employer liaises with your financial broker after the initial paperwork is complete and contributions are arranged from the agreed start date of the policy.

What happens if a member leaves employment?

If a member of an Executive Pension Plan decides to change employment, they have the option to transfer their pension plan. This means you can bring your Executive Pension Plan across to your new employment.

This flexibility is a huge plus and another incentive to use an Executive Pension Plan where possible. Should you run an Executive Pension Plan in your company, it also allows any new employees the opportunity to join.

Who owns the Executive Pension Plan?

An Executive Pension Plan is held in trust by the members of the scheme. Essentially, this means that neither the member nor the employer owns the scheme directly.

The Trustees of the scheme hold the legal responsibility to make sure the scheme is run correctly and that members receive benefits due.

In many cases, an employer will act as the trustee of the pension scheme. However, individuals may also act as Trustees.

In some cases, an Independent Trustee company may be appointed. Often these will be recommended by the life insurance company.

Are Small Self-Administered Pension Schemes different to Executive Pension Plans?

A Small Self-Administered Pension Scheme (SSAS) differs from an Executive Pension Plan.

Where a Small Self-Administered Scheme differs, is how and where the contributions are invested. With a Small Self-Administered Scheme, contributions are invested through a Pensioner Trustee company rather than through a life insurance company.

A major benefit of a Small Self-Administered Scheme over an Executive Pension is it may give you a wider choice of assets to invest in. If you feel you may be suitable for such a scheme, it may be worth consulting with an advisor.

Can the company receive corporation tax benefits from contributing to an Executive Pension Plan?

A company is eligible to receive corporation tax relief on Executive Pension Plan contributions within certain limits.

These contributions may be allowed as a deduction against profits from trading activities for Corporation Tax. In the case of a Sole Trader, you may be eligible to receive income tax relief.

An advantage of Executive Pension Plans is the ability it gives a company to make significant contributions to the plan.

Don't Get Left Behind!

We send out a short email every Thursday with some tips and information we think may be useful.

Join over 2,000 subscribers who enjoy our weekly tips!